Understandably, much of the attention related to cyber disclosures relate to how – and when – to make disclosure related to cyber incidents in a Form 8-K. But perhaps equally as important is consideration of what you should be disclosing…

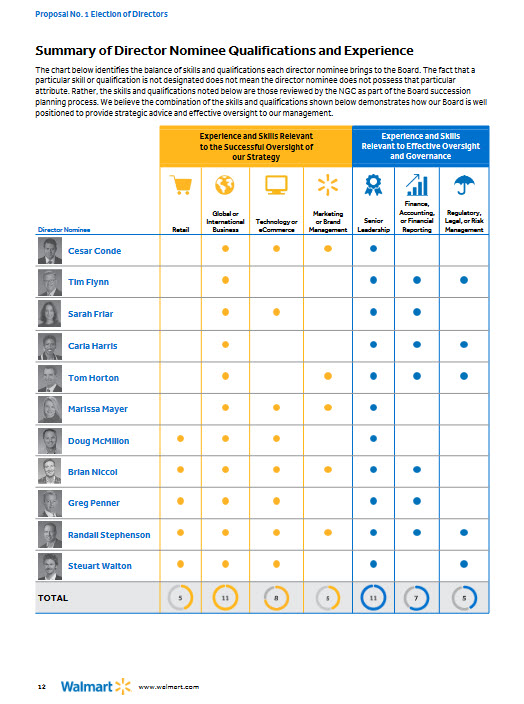

Last year, I blogged about the board skills matrix, highlighting a few of the Transparency Criteria that apply and noted a few good disclosure examples. I wanted to bring Wal-Mart’s 2024 proxy (on pages 11-12) to your attention because of…

Over the years, I’ve talked to a number of brilliant in-house disclosure drafters and a number of them have said that they go through the exercise of re-imaging a section in their proxy or 10-K that feels stale. Perhaps it’s…

At the Society of Corporate Governance conference last week, there was some talk about how some people think that too many shareholder proposals these days aren’t submitted with the intention of creating long-term value. This discussion was held during a…

In this 18-page thought piece, the Labrador team shares some thoughts for you to consider as you look to adopt a unified strategy for your corporate disclosures…

In this 30-page thought piece, Labrador discusses practice tips and ways to structure and present your code of conduct so that it is relevant and influential and, in turn, more effectively supports your compliance program and improves your overall messaging.…

Here is a list of 15 annual integrated reports from companies that are trying their best to be aligned – or inspired – with CSRD and ESRS, courtesy of Maria Tymtsias:

1. Metsä Group (Industry: Paper & Packaging)

2. H+H…

It might well be the case that many of you reading this don’t have any input into the IR web page at your company (or for your clients). When I was in-house, drafting the disclosure documents filed with the SEC,…

In this 12-page thought piece, Labrador discusses national and international trends on how racial and social justice movements have impacted ESG reporting best practices – including providing some good examples of recent disclosures. Labrador also offers suggestions for enhancing your…

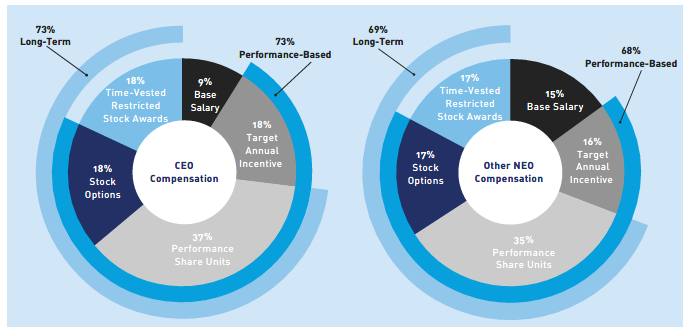

Transparency Criteria #66 for the proxy states: “The document includes disclosure of CEO and average NEOs pay mix presented as a graphic or using other visual elements.”

The “pay mix” graphic is designed to demonstrate that the CEO and other…

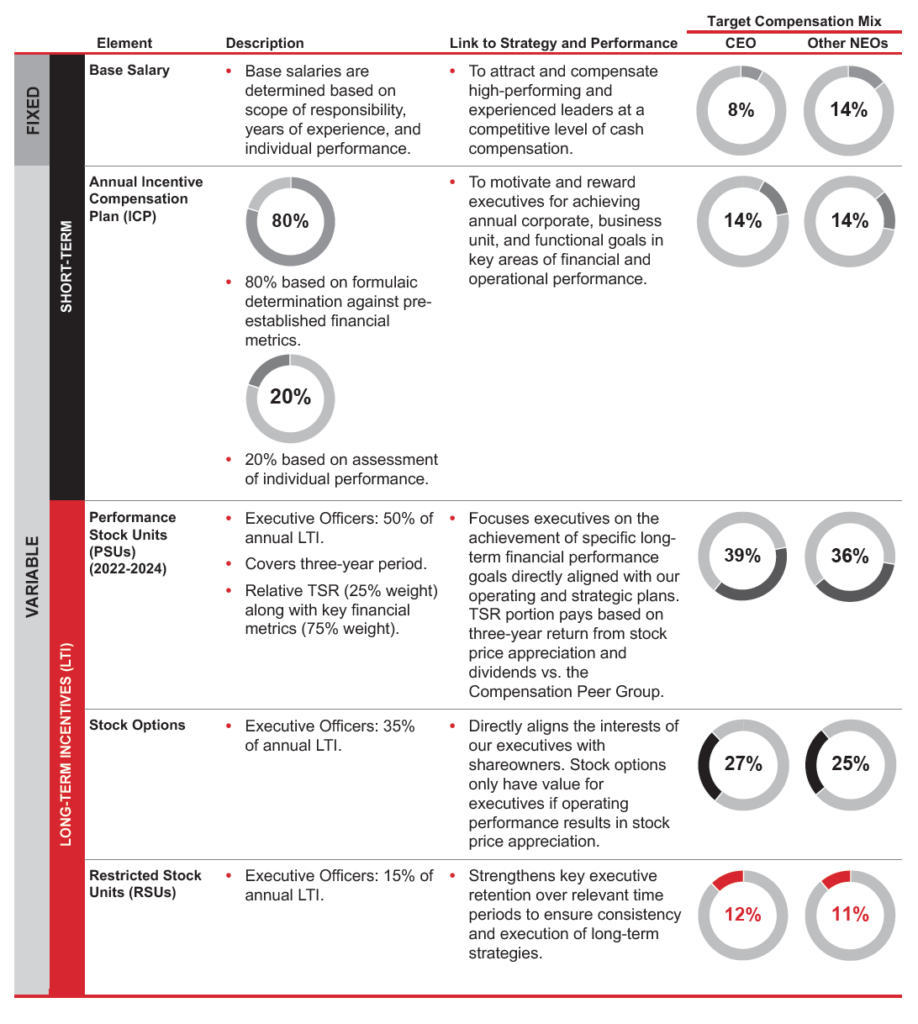

Following up on my recent blog about the “CD&A Executive Summary,” understanding the elements of a compensation program are so crucial that a good proxy summarizes this information at the outset. A reader wants to know what your elements are,…

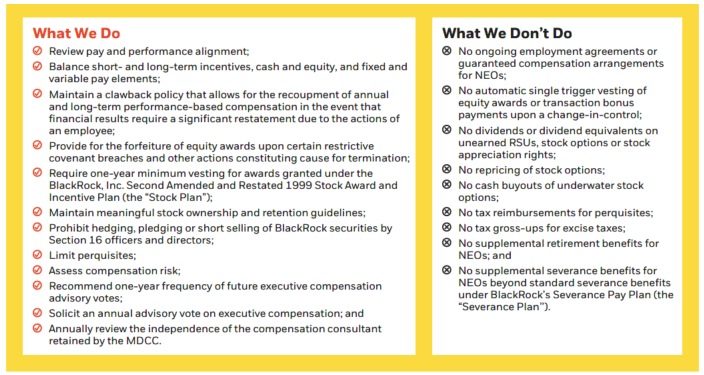

Transparency Criteria #63 for the proxy states:

The proxy summary or CD&A executive summary includes a summary of key compensation practices and policies (what we do/don’t do, or list).

As a long-time practitioner, it’s been interesting to see the phenomenal…

Since the SEC last overhauled its executive pay disclosure requirements in 2006, there’s been a slow and steady change in the ways that compensation matters have been disclosed in the proxy. One of those changes is the need for a…

At the present time, our set of transparency criteria doesn’t address the “statements in opposition” to shareholder proposals that companies include in their proxies after each shareholder proposal included in their proxy. In his recent “Shareholder Service Optimizer” article, long-time…

In this 20-page thought piece, Labrador explores different ways that companies should show off their directors, as well as show a comprehensive director nomination process, link skills to strategy, bring focus to the relevance of a director’s skill and more…